Global S&T Development Trend Analysis Platform of Resources and Environment

| Energizing Renewables in Indonesia: Optimizing Public Finance Levers to Drive Private Investment | |

| Randy Rakhmadi; Alke Haesra and Muhammad Ery Wijaya | |

| 2018-12 | |

| 出版年 | 2018 |

| 语种 | 英语 |

| 国家 | 美国 |

| 领域 | 气候变化 |

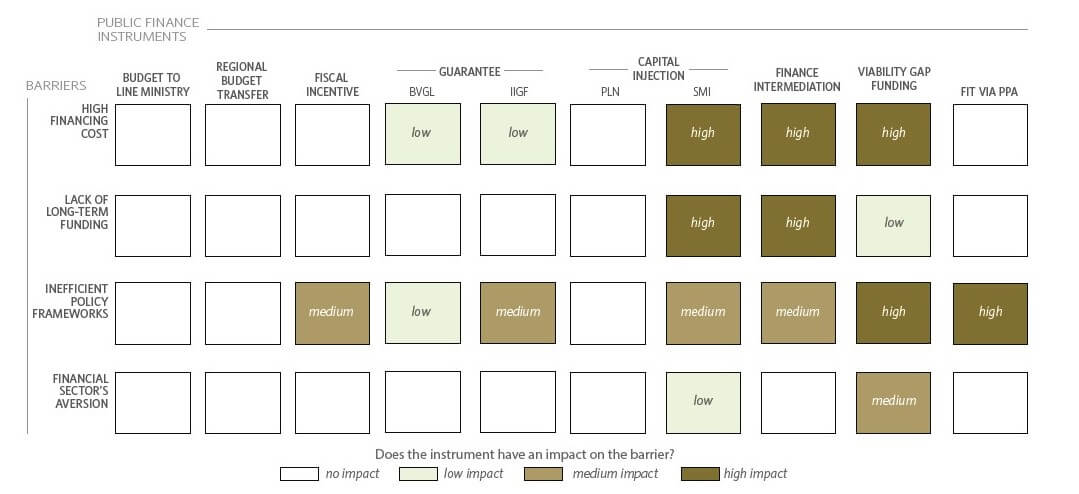

| 英文摘要 | Transforming Indonesia’s energy sector is becoming increasingly important to achieve the country’s climate goals. According to the country’s Nationally Determined Contribution (NDC) under the Paris Agreement, Indonesia seeks to reduce 834 MT CO2 emissions by 2030, 38% of which will come from reduced energy emissions. This is not only an ambitious target, but a significant increase in energy emissions reductions from previous climate change mitigation commitments. These targets will ultimately require increased use of clean energy for power generation, and indeed, Indonesia seeks to achieve 23% renewable share in its primary energy mix by 2025. The current share of renewable energy, however, is less than 8%. This means that Indonesia will need to quickly pick up the pace if it is to achieve these goals in the next six years. And while different sources of renewable energy in Indonesia hold great potential, none have been utilized at significant levels to-date. In 2017, renewable energy capacity only reached 6.3 GW of the total target capacity of 45.2 GW in 2025. Finance for renewable energy generation will be a key driver to help Indonesia meet its clean energy goals. PLN, the state electricity company, estimates that the total investments needed to reach renewable energy targets is IDR 2,000 trillion, or equivalent to USD 154 billion (PLN, 2016). For power generation alone, investment needs amount to IDR 1,400 trillion, or an average of IDR 140 trillion per year. To meet this target, the Government of Indonesia needs to attract other sources of finance, particularly from private actors. Blended finance instruments, which make use of public and/or philanthropic funds to mobilize multiples of additional private capital (Tonkonogy et al., 2018), offer promising finance structuring solutions to address the risks and barriers to clean energy investment. Around the world, blended finance offers more than USD 1 trillion in investment opportunities for clean energy. This report presents the findings from the first study in a series of reports by Climate Policy Initiative Indonesia in partnership with the Indonesian Ministry of Finance that look at national opportunities for blended finance. In particular, this study aims to understand the role of public finance instruments for clean energy and identify opportunities to optimize them to spur private investment in Indonesia. The ultimate objective is to inform Indonesia’s public resource allocation strategy so that it will address the most critical barriers to The key findings of the study are as follows: Public finance instruments have different roles in supporting clean energy deployment, and some are more effective in catalyzing private investment than others. Our assessment based on the finance provided in the period of 2012-2016 indicates that guarantees and capital injections to state-owned enterprise have the highest impact for leveraging private investment. On the other hand, budget appropriations to line ministries and fiscal transfers to regional governments show no direct impact to address private sector barriers to renewable energy investments. Fittingly, these instruments are typically deployed to support small-scale renewable projects in remote areas in which private investment interest is absent. There are opportunities for public finance instruments to further address financing barriers, thereby helping unlock private capital and growing the clean energy market in Indonesia.

These barriers are spread across the life cycle of clean energy projects, making the case for more strategic use of public finance instruments to accelerate private participation in clean energy. Figure 1 summarizes which public finance instruments have the most potential for addressing each financing barrier. Fiscal incentives have good potential to improve the risk-return profile of medium-to-large scale renewable energy projects. A lower tax rate or deferred tax expenses can both directly lower generation costs and improve the risk-return profile for the project developer. Guarantee instruments channeled through business viability guarantee letter (BVGL) and Indonesia Infrastructure Guarantee Fund (IIGF) primarily focus on public sector performance, BVGL is key to guarantee PLN’s business viability and its ability to fulfill its financial obligation, both as an off-taker and borrower. IIGF covers political and public-sector performance risk in infrastructure projects under a Public Private Partnership (PPP) scheme. The coverage of risks by these instruments, which so far are still limited, have the potential to be expanded. The government’s capital injection to PLN (state electricity company) and SMI (local development financial institution) are critical to strengthen the financial foundations of these public companies but have different impacts in terms of addressing barriers to private investment. Capital injection to PLN provides a more minor impact as most power plants developed by PLN are wholly-owned by PLN. In contrast, capital injections to SMI have high impact potential because, as a quasi development financial institution, SMI has the capacity to blend capital provided by the government with external sources of capital and the flexibility to develop financial instruments to meet the needs of renewable energy projects. Finance intermediation also has high potential to address many private sector financing challenges, particularly if channeled through domestic public financial institutions, like SMI and its subsidiary, Indonesia Infrastructure Finance. These instruments typically channel funds from multilateral organizations which, through their excellent credit rating, have the ability to raise and provide low-cost funding with more flexible terms compared to what the recipients would be able to get in the financial market. Viability Gap Funding (VGF) has high potential application in addressing high financing cost and in improving the risk-return profile of large-scale projects but so far it has not been provided for clean energy projects. VGF, typically in the form of grant support that does not require financial return, is provided to support infrastructure projects that are economically and technically feasible but lack commercial viability. VGF is available only to projects developed under PPP scheme, and hence, typically only to large-scale projects. Feed-in-Tariff (FiT) has high potential in improving the risk-return profile of renewable energy projects. FiT influences the only source of revenue for renewable energy project financiers. FiT is regulated by the Ministry of Energy and Mineral Resources and implemented through Power Purchase Agreement between PLN and Independent Power Producers. Recommendations Provide sufficient revenue support Expand the role of local development financial institutions Direct public finance to address critical early-stage project development risks Expand guarantee coverage and increase focus on climate-related projects |

| 英文关键词 | clean energy climate finance climate policy renewable energy |

| URL | 查看原文 |

| 来源平台 | Climate Policy Initiative |

| 文献类型 | 科技报告 |

| 条目标识符 | http://119.78.100.173/C666/handle/2XK7JSWQ/242554 |

| 专题 | 气候变化 |

| 推荐引用方式 GB/T 7714 | Randy Rakhmadi,Alke Haesra and Muhammad Ery Wijaya. Energizing Renewables in Indonesia: Optimizing Public Finance Levers to Drive Private Investment,2018. |

| 条目包含的文件 | 下载所有文件 | |||||

| 文件名称/大小 | 文献类型 | 版本类型 | 开放类型 | 使用许可 | ||

| Energizing-Renewable(505KB) | 科技报告 | 开放获取 | CC BY-NC-SA | 浏览 下载 | ||

除非特别说明,本系统中所有内容都受版权保护,并保留所有权利。

修改评论